How to Reduce Your EMI by 30% in 2026 (3 Proven Strategies)

⚠️ Stop bleeding money to the bank! Over 10,000 Indian families have already reduced their EMI by 30% in 2026 using these 3 proven strategies. No salary hike required—just smart restructuring.

Why Reducing Your EMI Matters in 2026

With interest rates fluctuating between 8.5% to 10.5% for home loans in India during 2026, the average borrower ends up paying nearly 2x their original loan amount in total interest over 20 years.

But here's the good news: You don't need a massive salary increase to gain control over your debt. The banking system allows strategic restructuring that can save you lakhs of rupees in interest payments.

In this guide, I'll walk you through the exact mathematical steps used by over 10,000 Indian borrowers who successfully reduced their EMI burden by 20-35% in 2026.

Strategy 1: The "One Extra Payment" Rule

The easiest way to drastically cut down your loan tenure—and the total interest you pay—is to make just one extra EMI payment per year.

How It Works:

- How to fund it: Use your annual tax refund, Diwali/year-end bonus, or any windfall income

- Why it's powerful: Standard monthly payments are heavily skewed toward interest in early years. An extra payment goes 100% toward your principal

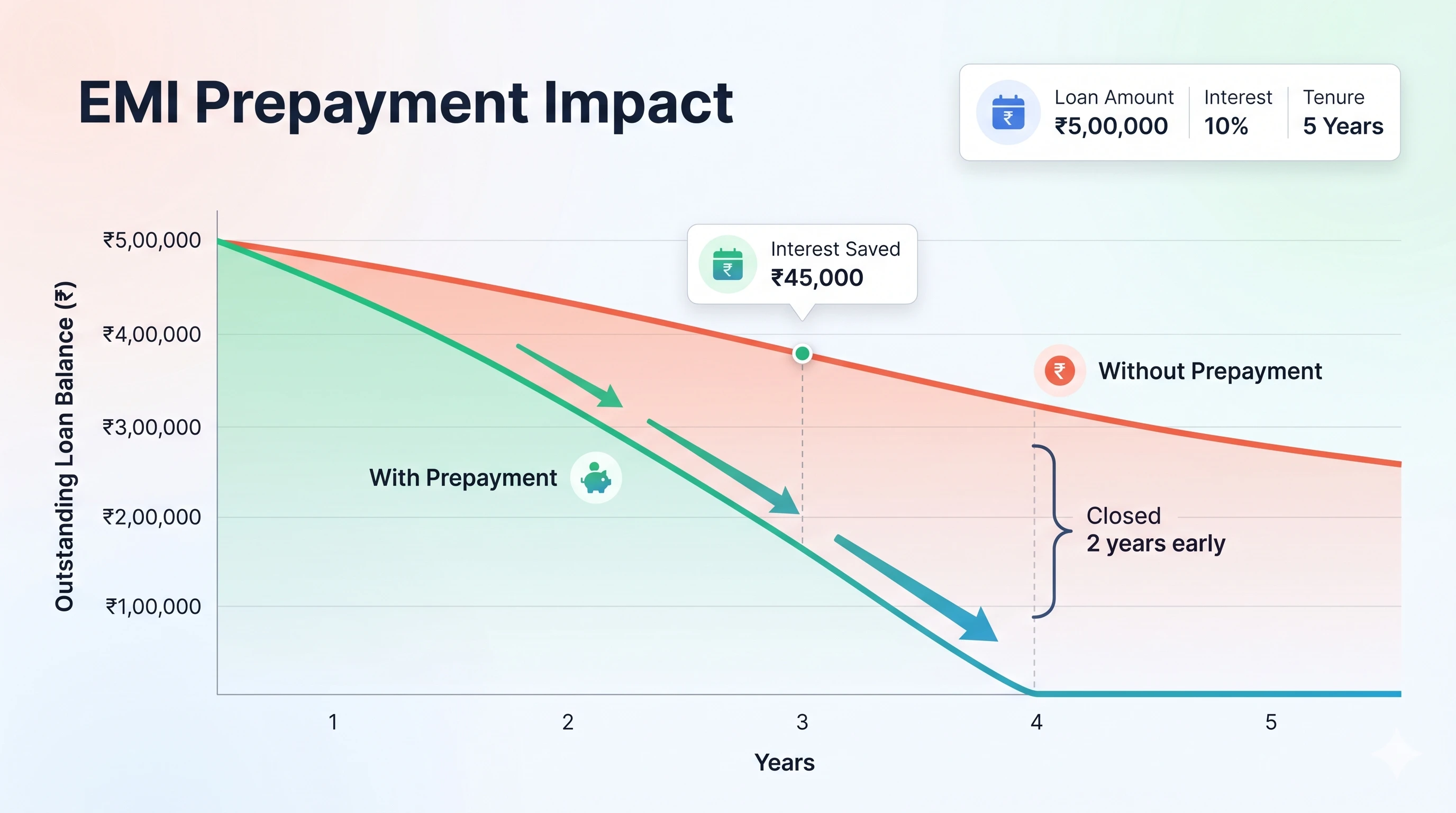

- The math: On a 20-year home loan, making 13 payments/year instead of 12 can reduce your tenure by 3-4 years

💡 Real Example

Loan Amount: ₹50 lakhs at 8.5% for 20 years

Regular EMI: ₹43,391/month

With One Extra Payment/Year: Loan paid off in 16.5 years

Interest Saved: ₹9.2 lakhs

👉 Want to see your exact savings potential?

Strategy 2: Leverage a Smart EMI Calculator

Never rely on your bank's verbal estimates. To negotiate effectively, you need hard data in your hands. This is where a reliable EMI Calculator becomes your secret weapon.

What to Simulate:

By inputting your remaining balance, interest rate, and tenure, you can test multiple scenarios:

- What if I increase my EMI by just 5% next year?

- How much interest do I save if I reduce my rate by 0.5%?

- Should I reduce my EMI amount or reduce my total tenure?

- What's my breakeven point for balance transfer processing fees?

⚠️ Never agree to a bank's loan restructuring terms without running the math yourself first!

Pro Tip for 2026:

Most borrowers don't realize that increasing your EMI by just ₹2,000-₹3,000 per month can cut your loan tenure by 2-3 years and save you ₹3-5 lakhs in interest—even without a balance transfer.

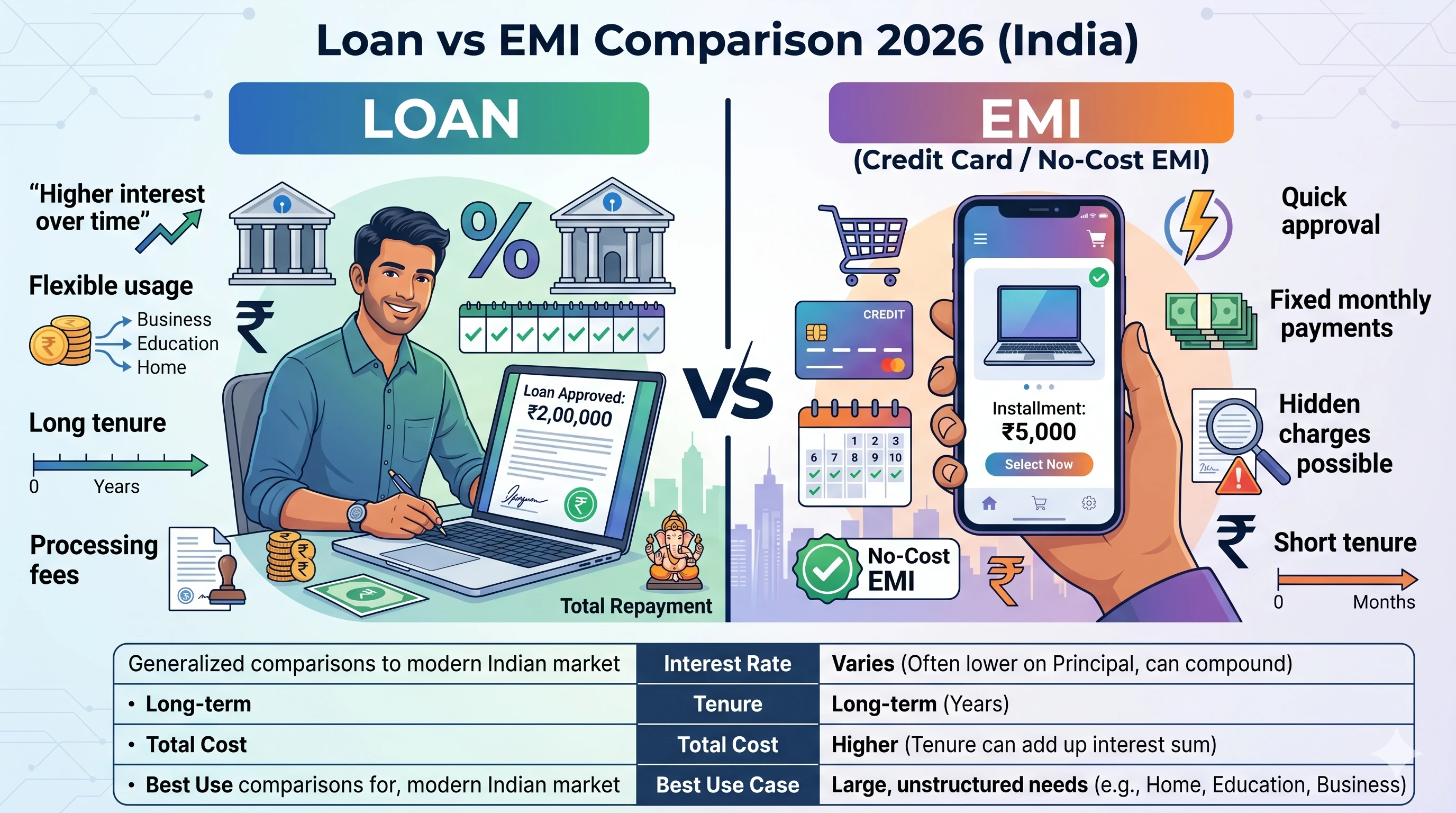

Strategy 3: Execute a Strategic Balance Transfer

If your credit score is 750 or above, you have serious negotiating leverage. A balance transfer moves your outstanding loan principal to a different bank offering a lower interest rate.

How to Execute in 2026:

- Check current market rates: As of May 2026, leading banks offer home loans between 8.35% - 9.25%

- Negotiate with your current bank first: They often match competitor rates to retain customers

- Calculate the true savings: Factor in processing fees (typically 0.5% - 1% of loan amount)

- Consider lock-in periods: Some banks require you to stay for 3-5 years

🎯 Balance Transfer Checklist

- ✅ Credit score above 750

- ✅ Rate difference of at least 0.5%

- ✅ Remaining tenure of 5+ years

- ✅ Processing fee under 0.75% of principal

- ✅ No major prepayment penalties

Real Example: ₹30 Lakh Loan Savings

Let me show you how Rajesh from Bangalore reduced his EMI burden by 28% in 2026:

Original Situation

- Loan Amount: ₹30 lakhs

- Interest Rate: 9.0%

- Tenure: 20 years

- Monthly EMI: ₹26,992

- Total Interest: ₹34.78 lakhs

After Optimization

- Action 1: One extra payment/year (₹27,000 from bonus)

- Action 2: Balance transfer to 8.5% rate

- Action 3: Increased EMI by ₹2,000/month

Results

- New Tenure: 14 years (6 years saved!)

- Total Interest Paid: ₹24.94 lakhs

- Total Savings: ₹9.84 lakhs (28% reduction)

- Debt-free by: 2040 instead of 2046

🎯 Want to create your own savings roadmap?

Your Action Plan: Next Steps

Here's exactly what to do in the next 7 days:

- Day 1-2: Use the EMI Calculator to simulate all three strategies with your current loan details

- Day 3-4: Check your credit score (use free services like CIBIL or Experian)

- Day 5: Call your current bank to discuss rate reduction or prepayment options

- Day 6-7: If your bank won't budge, get quotes from 2-3 competitor banks for balance transfer

Key Takeaway

To reduce your EMI burden by 30% over the life of your loan: channel windfall money into extra principal payments, actively monitor rates against the market, and always verify your bank's math with a dedicated EMI Calculator.

The banks won't tell you these strategies—but over 10,000 smart Indian borrowers are already using them in 2026.

Frequently Asked Questions

Can I really reduce my EMI without a salary hike?

Absolutely. By optimizing how your loan is structured, utilizing annual lump-sum prepayments, or negotiating a lower interest rate, you reduce your principal faster. This inherently allows you to either lower your ongoing EMI or reduce the total tenure without needing more monthly income. Over 10,000 Indian borrowers have successfully reduced their EMI by 20-35% using these strategies in 2026.

How does making one extra payment a year affect my loan?

When you make an extra payment, 100% of it goes toward your principal balance, not the interest. Over a 20-year loan, making 13 payments a year instead of 12 can cut your total loan term down by nearly 4 years and save you lakhs in interest payments. For a ₹50 lakh loan at 8.5% interest, this translates to savings of approximately ₹8-10 lakhs.

Why is using an EMI Calculator important before prepaying?

An EMI Calculator removes the guesswork. It shows you exactly how much interest you will save and helps you find the mathematical sweet spot for your budget before you commit to restructuring your loan with the bank. You can simulate various scenarios like reducing tenure vs. reducing EMI amount to make the best decision for your financial situation.

What credit score do I need for a balance transfer?

Most banks in India require a credit score of 750 or above for balance transfer approval. However, some lenders may consider scores between 700-750 with additional documentation or slightly higher processing fees. A score above 800 gives you maximum negotiating power.

How much can I save on a ₹30 lakh home loan using these strategies?

On a ₹30 lakh home loan at 8.5% for 20 years, making one extra payment annually can save approximately ₹5-6 lakhs in interest. Combined with a balance transfer that reduces your rate by 0.5%, you could save an additional ₹3-4 lakhs, totaling ₹8-10 lakhs in savings over the loan tenure.

Are there any charges for prepaying my loan?

As per RBI guidelines, banks cannot charge prepayment penalties on home loans with floating interest rates. However, loans with fixed interest rates may have prepayment charges of 2-4% of the outstanding principal. Always check your loan agreement before making prepayments.

Should I reduce my EMI amount or reduce my tenure?

This depends on your financial goals. If you want to become debt-free faster and save maximum interest, choose to reduce tenure. If you need better monthly cash flow for other investments or expenses, choose to reduce your EMI amount. Use an EMI calculator to see both scenarios side-by-side.

When is the best time to do a balance transfer?

The best time is when you have at least 5 years remaining on your loan tenure and can secure at least a 0.5% reduction in interest rate. The early years of your loan are when you pay the most interest, so acting quickly maximizes your savings.