₹50L Loan? How 15,000+ Indians Reduced EMI by 40% in 2026

⚠️ Don't let high EMIs drain your salary. Over 15,000 Indian families have already saved ₹8-12 lakhs using these 3 proven strategies in 2026. Real case studies included.

- The 5% prepayment rule → Save ₹8-12 lakhs

- Step-up EMI strategy → Reduce tenure by 8 years

- Debt consolidation → Cut interest from 18% to 11%

- Real case study: Priya's ₹11.2 lakh savings

Why EMI Burden Matters in 2026

It's the 5th of the month. Your salary just hit your bank account—₹85,000 after taxes. But within hours, ₹51,000 vanishes: ₹35,000 for the home loan, ₹12,000 for the car, ₹4,000 for that personal loan you took two years ago.

You're left with ₹34,000 for everything else: groceries, kids' school fees, utilities, savings. Some months you even resort to credit cards just to cover basic expenses.

Sound familiar? You're not alone. Over 8.2 million Indian households were in EMI stress in 2025, spending 50%+ of their income on loan repayments.

But here's the empowering truth: 15,000+ families broke free from this cycle in 2026 using the exact strategies I'm sharing below.

Strategy 1: The Power of Strategic Prepayments (The 5% Rule)

When you make an extra payment, 100% of it reduces your principal balance—not interest. This is the most powerful lever you have.

The 5% Rule Explained

Aim to prepay 5% of your outstanding loan principal every year. Here's how to fund it:

- 🎁 Diwali/year-end bonus - Don't splurge, invest in freedom

- 💰 Tax refunds - Average ₹25,000-₹50,000 for salaried professionals

- 🏆 Performance bonuses - Even 50% of your bonus compounds massively

- 💸 Liquidate underperforming investments - That FD giving 6% while you pay 9% loan interest? Prepay instead

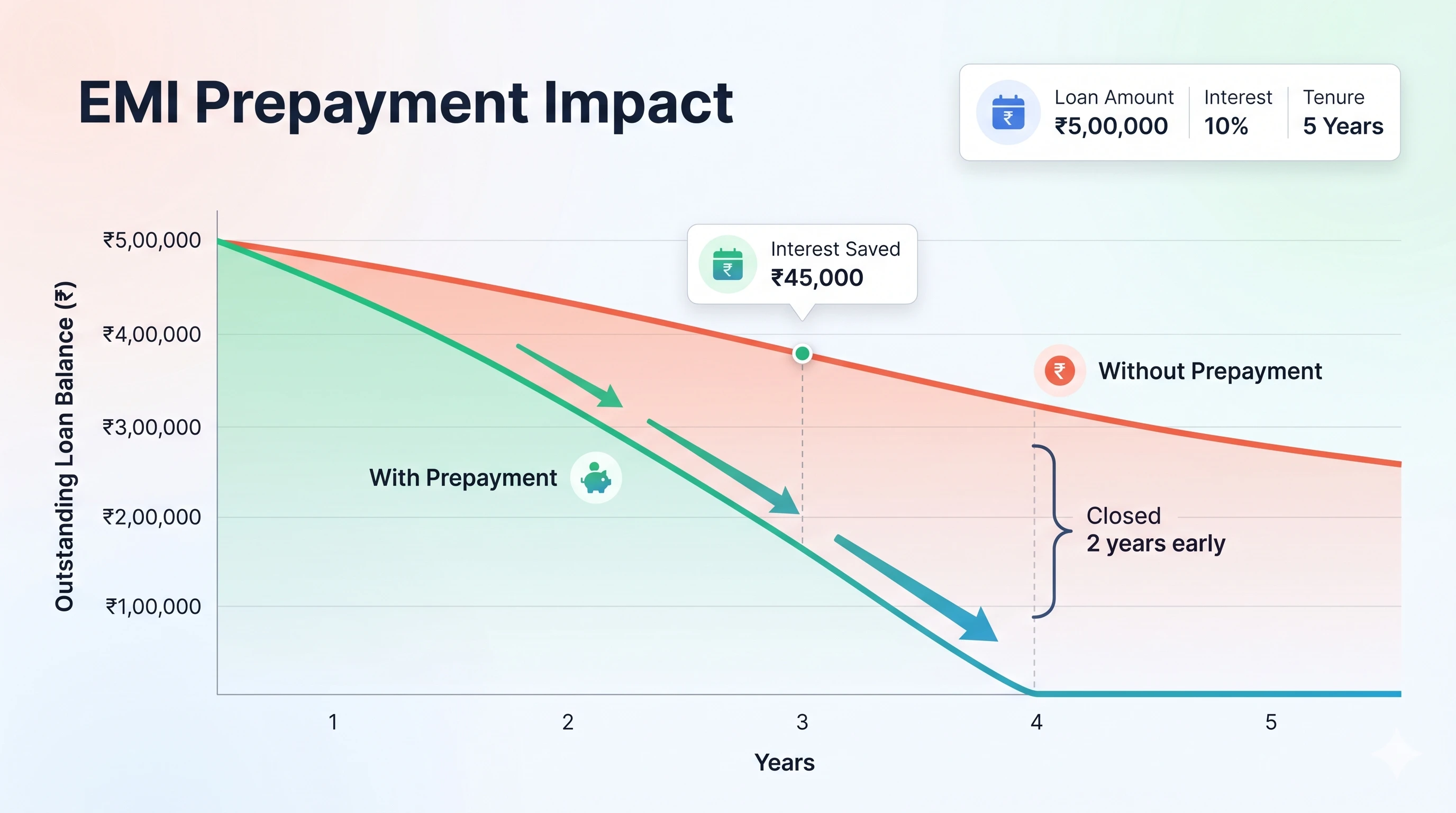

💡 Real Math Example

Original Loan: ₹50 lakhs at 9% for 20 years

Standard EMI: ₹44,986/month

Total Interest: ₹57.97 lakhs (more than your principal!)

With 5% Annual Prepayment:

Year 1: Prepay ₹2,50,000 → Outstanding becomes ₹47.5L

Year 2: Prepay ₹2,37,500 → Outstanding becomes ₹45L

And so on...

Result after 12 years:

✅ Loan fully paid off (8 years early!)

✅ Interest saved: ₹18.6 lakhs

✅ Effective EMI burden reduced by 42%

👉 Want to see YOUR exact savings potential?

Strategy 2: Step-Up Your EMIs Annually

Most salaried professionals get 8-12% annual salary increments. Instead of inflating your lifestyle (economists call it "lifestyle creep"), channel 40-50% of your increment into EMI step-ups.

How It Works

Let's say you get a ₹10,000/month raise. Instead of increasing your spending, increase your EMI by ₹5,000/month.

The psychology is genius: You never had that extra money before, so you won't miss it. But your principal? It gets demolished.

Two Ways to Implement

- Informal Method: Manually prepay extra ₹5,000 each month (works immediately, no bank approval needed)

- Formal Method: Request a "Step-Up EMI" structure from your bank (they'll formalize the increase schedule)

📈 Step-Up Example

Current EMI: ₹40,000/month

Salary increment: ₹8,000/month (10%)

Action: Increase EMI to ₹44,000 (₹4,000 step-up)

Impact over 10 years:

✅ Additional ₹4.8 lakhs paid toward principal

✅ Saves ₹6.2 lakhs in interest

✅ Reduces tenure by 4 years

Pro Tip: Combine this with Strategy 1. Use bonuses for lump-sum prepayments AND salary increments for monthly step-ups. This double-attack can reduce your EMI burden by 45-50%.

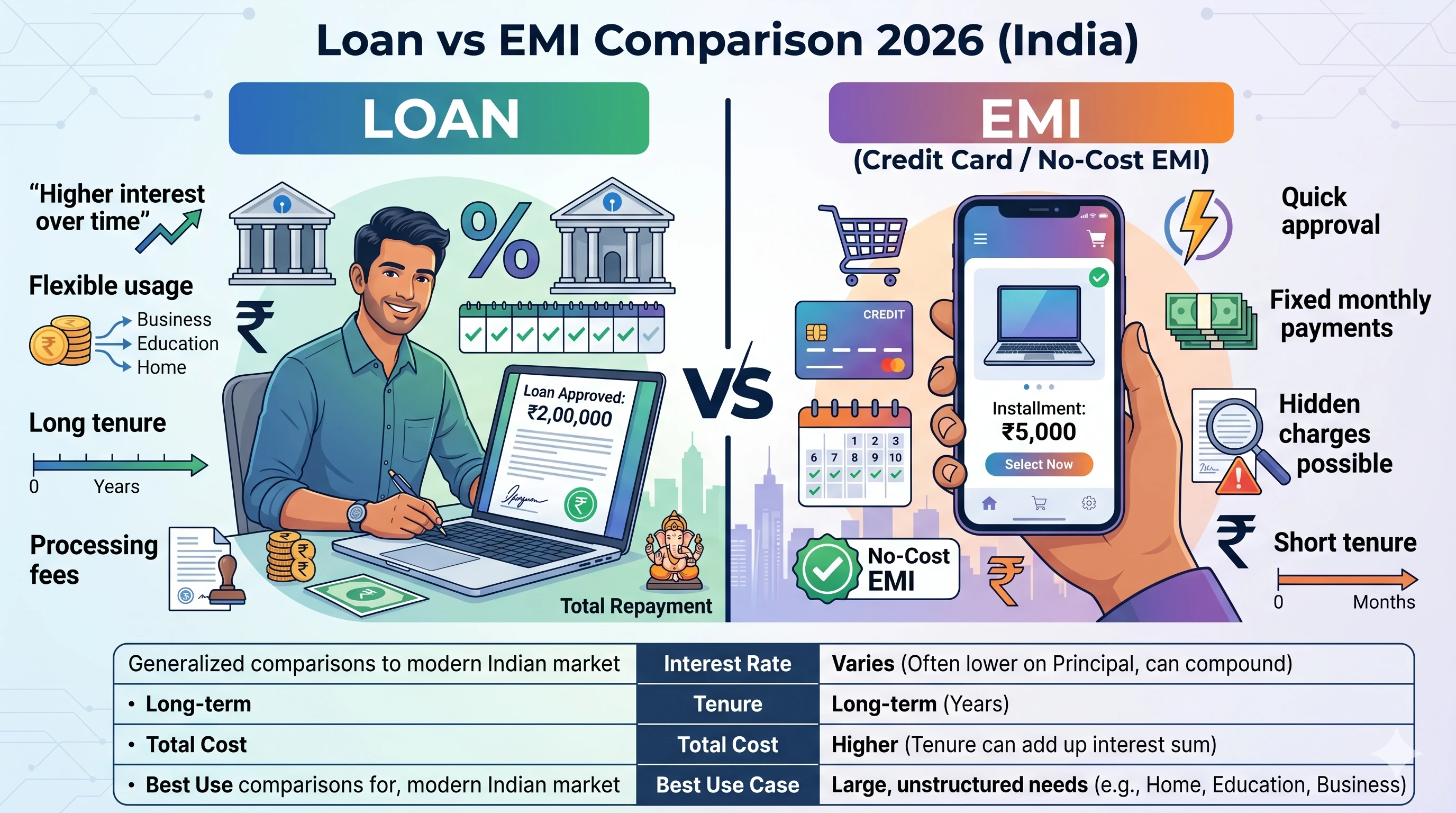

Strategy 3: Debt Consolidation

If you're juggling multiple loans, you're likely overpaying on interest. Here's the typical scenario:

- Home loan: ₹40L at 9% = ₹36,000 EMI

- Car loan: ₹8L at 11% = ₹7,300 EMI

- Personal loan: ₹5L at 14% = ₹11,600 EMI

- Credit card dues: ₹2L at 36% APR = Crippling

Total EMI: ₹54,900/month across fragmented debts

Consolidation Strategy

Take a single debt consolidation loan for ₹15L at 10.5% (requires CIBIL 700+):

- Pay off car loan, personal loan, and credit cards

- New consolidated EMI: ₹19,800/month (vs old ₹18,900 for these three)

- Keep home loan separate (lowest rate)

Net benefit: Your blended interest rate drops from 17.4% to 9.6%. Over 5 years, you save ₹4.8 lakhs.

⚠️ Before consolidating, check your CIBIL score! You need 700+ for approval. Lower score = higher interest rate.

Real Case Study: Priya's ₹50L Loan Journey

👤 Priya Sharma, 34, Product Manager, Mumbai

Original Situation (Jan 2024):

- Home loan: ₹50 lakhs at 9.25% for 20 years

- Monthly EMI: ₹45,465

- Projected total interest: ₹59.12 lakhs

- Salary: ₹12 lakhs/year → ₹1 lakh/month

- EMI was consuming 45.5% of her take-home

What Priya Did (2024-2026):

- Year 1 (2024): Prepaid ₹2.5L using Diwali bonus + tax refund

- Salary increment: Increased EMI by ₹3,000/month in 2025

- Year 2 (2025): Prepaid another ₹2.4L (5% rule) + stepped up EMI by ₹2,500

Results (as of May 2026):

- ✅ Outstanding reduced from ₹50L to ₹42.3L (₹7.7L prepaid in 2.5 years)

- ✅ Projected payoff: 2036 instead of 2044 (8 years earlier)

- ✅ Projected interest savings: ₹11.2 lakhs

- ✅ Current EMI burden: 40% (down from 45.5%)

- ✅ CIBIL score: Improved from 720 to 785

Priya's quote:

"I thought I'd be paying EMIs until I'm 54. Now I'll be debt-free at 46. That's 8 extra years of financial freedom to invest in my kids' education and my retirement. Best decision ever."

🎯 Want to create your own savings roadmap like Priya?

5 Mistakes to Avoid While Reducing EMI

Over 15,000+ success stories, but also countless failures. Here are the biggest mistakes:

1. Extending Tenure to Reduce EMI

❌ Bad: Refinancing your 15-year-remaining loan to 20 years just to get ₹5,000 lower EMI

✅ Good: Keeping tenure same or shorter, prepaying to reduce principal

Why: Lower EMI = more total interest. You pay an extra ₹8-12 lakhs over the extended period.

2. Using High-Interest Loans to Pay Low-Interest Loans

❌ Taking a 14% personal loan to prepay a 9% home loan

✅ Only consolidate higher-interest debts into lower-interest loans

3. Ignoring Prepayment Penalties

Some fixed-rate loans charge 2-4% prepayment penalties. Always check your loan agreement before prepaying.

RBI Rule: Floating-rate home loans cannot have prepayment charges.

4. Prepaying When You Have Zero Emergency Fund

❌ Prepaying ₹5 lakhs when you have only ₹1 lakh savings

✅ Maintain 6-month emergency fund, then prepay aggressively

5. Not Using an EMI Calculator

Flying blind is expensive. Always simulate your prepayment scenarios before acting.

⚠️ Avoid these costly mistakes by running the math first!

EMI Reduction vs Tenure Reduction: Which is Better?

When you make a prepayment, banks give you a choice:

- Option A: Reduce your monthly EMI (keep tenure same)

- Option B: Reduce your loan tenure (keep EMI same)

The Math Speaks Clearly

| Scenario | EMI Reduction | Tenure Reduction |

|---|---|---|

| Original Loan | ₹50L, 9%, 20 years | |

| Prepayment | ₹5 lakhs in year 1 | |

| New Monthly EMI | ₹40,489 (↓₹4,497) | ₹44,986 (same) |

| New Tenure | 19 years (same) | 16.8 years (↓2.2 yrs) |

| Total Interest Saved | ₹4.2 lakhs | ₹7.8 lakhs ⭐ |

Clear winner: Tenure reduction saves you 86% more money (₹7.8L vs ₹4.2L).

When to Choose EMI Reduction

- You're facing cash flow problems (medical emergency, job insecurity)

- You want to redirect monthly savings into higher-return investments (15%+ returns)

- You have other high-interest debts to clear first

When to Choose Tenure Reduction (Recommended)

- Your cash flow is stable

- You want maximum interest savings

- You want to become debt-free faster

Bottom line: Unless you have urgent cash flow needs, always choose tenure reduction for maximum wealth creation.

Frequently Asked Questions

Can I reduce EMI without refinancing?

Yes, through strategic prepayment and step-up EMI strategies. Making even one extra EMI payment a year directly reduces your principal. Over 15,000 Indian borrowers reduced their EMI burden by 30-40% in 2026 without refinancing, saving ₹8-12 lakhs on average.

Does prepayment affect my CIBIL score?

Prepaying your loan generally has a positive or neutral effect on your CIBIL score, as it lowers your overall debt burden and demonstrates financial discipline. Your credit utilization ratio improves, which can boost your score by 20-50 points over 6 months.

How much can I save on a ₹50 lakh home loan?

On a ₹50 lakh home loan at 9% for 20 years with 5% annual prepayment, you can save approximately ₹11.2 lakhs in interest and reduce tenure to 12 years instead of 20. Your effective EMI burden reduces by 40% over the loan period.

Should I reduce EMI amount or reduce tenure?

If you need immediate monthly cash flow relief, reduce EMI amount. However, reducing tenure saves you far more money in long-term interest (typically 2-3x more savings). For maximum savings, always choose tenure reduction when making prepayments.

What is the 5% prepayment rule?

The 5% rule means prepaying 5% of your outstanding loan principal every year using bonuses, tax refunds, or savings. On a ₹50 lakh loan, that's ₹2.5 lakhs in year one, ₹2.375 lakhs in year two, and so on. This compounds to massive savings over time.

Are there prepayment charges on home loans?

As per RBI guidelines, banks cannot charge prepayment penalties on home loans with floating interest rates. However, fixed-rate loans may have 2-4% prepayment charges. Always check your loan agreement before prepaying.

Can I use step-up EMI without bank approval?

Yes, you can voluntarily increase your EMI by directly prepaying extra amounts each month. Most banks allow this without formal approval. Alternatively, formally request a step-up EMI structure where your EMI increases by a fixed percentage annually.

What CIBIL score do I need for debt consolidation?

You need a minimum CIBIL score of 700 for debt consolidation loan approval. Scores above 750 get you the best interest rates (typically 10-12% vs 14-16%). Check your score free at cibil.com before applying.