Personal Loan vs No-Cost EMI (2026): Which Actually Saves You ₹10,000?

⚠️ Most Indians lose ₹5,000–₹20,000 by choosing the wrong financing option. Are you really saving money with a No-Cost EMI, or is it a disguised interest trap?

TL;DR: A No-Cost EMI is mathematically cheaper for direct product purchases, but hidden GST and processing fees will still cost you an extra ₹500 to ₹4,000. For direct cash needs or debt consolidation, a Personal Loan is required.

Before you commit to a major purchase in 2026—whether it is a new flagship smartphone, a home renovation, or paying off a sudden medical bill—you must mathematically calculate the true cost of your financing options. If you already have existing loans, adding more debt might require you to read our strategic guide on how to reduce your EMI burden by 40% first.

- No-Cost EMIs are NOT free: Expect to pay processing fees and 18% GST on hidden interest.

- Merchant discounts: In an EMI scheme, the retailer subsidizes the base interest, making it cheaper for product purchases.

- Personal Loans offer flexibility: Use them for debt consolidation or cash needs, not retail shopping.

| Financing Option | Best Suited For |

|---|---|

| No-Cost EMI | Buying specific retail products (Phones, Laptops) |

| Personal Loan | Direct cash needs & debt consolidation |

👉 Want to compare exact monthly payments? Use our Free EMI Calculator here.

The "No-Cost EMI" Truth: Exposing the Hidden Fees

E-commerce platforms prominently display "No-Cost EMI" banners, but according to the Reserve Bank of India (RBI) regulations on digital lending, banks are strictly prohibited from offering genuine 0% interest loans. So, how does this legally work?

To create a "No-Cost" illusion, the retailer gives you an upfront discount on the product equal to the interest the bank will charge over the EMI tenure. For a ₹1,00,000 product, the retailer bills you ₹90,000, and the bank charges ₹10,000 in interest, bringing your total outflow to ₹1,00,000.

However, the math is not perfectly clean. Banks will levy an EMI Processing Fee (typically ₹199 to ₹999), and the government requires you to pay 18% GST on the interest component. You are paying tax on money you supposedly weren't charged.

| Component | Cost for ₹1 Lakh Purchase |

|---|---|

| Product Price (Discounted) | ₹90,000 |

| Bank Interest (e.g., 15% p.a.) | ₹10,000 |

| GST on Interest (18%) | ₹1,800 |

| Processing Fee (incl. GST) | ₹590 |

| Total Actual Outflow | ₹1,02,390 |

Example: ₹50,000 Smartphone Purchase

Let's look at a smaller purchase. You buy a ₹50,000 phone on a 6-month "No-Cost" EMI. The bank charges 15% interest (approx ₹2,200), which the merchant discounts. But you still pay a ₹199 processing fee + 18% GST (₹35) and 18% GST on the ₹2,200 interest (₹396). The "free" EMI just cost you an extra ₹630 out of pocket.

Advanced Example: ₹2,00,000 Home Appliance Bundle (12 Months)

When you scale up to a ₹2 Lakh purchase over a 12-month tenure, the hidden costs magnify. At a 15% interest rate, the bank charges approximately ₹16,600 in interest (which the merchant discounts). However, you now pay 18% GST on that ₹16,600 (amounting to almost ₹3,000) plus a higher processing fee slab (e.g., ₹999 + GST). The "No-Cost" label actually carries nearly ₹4,180 in non-refundable taxes and banking fees.

Why Banks and Retailers Desperately Want You to Choose No-Cost EMIs

You might wonder why financial institutions heavily market a product where the interest is supposedly discounted. The reality is a masterpiece of financial engineering:

- Guaranteed Processing Revenue: Banks collect non-refundable processing fees instantly upfront, regardless of whether you prepay the loan later.

- The GST Loophole: The government collects 18% GST on the base interest amount. Since you bear this tax burden, the bank loses nothing.

- Merchant Volume: Retailers willingly absorb the base interest cost because offering a No-Cost EMI increases their sales volume and average order value (AOV) by over 30%.

- The Default Trap: Statistically, a percentage of users will miss an EMI payment, instantly triggering standard credit card interest rates of 40%+ on the entire remaining balance.

⚠️ If you skip the EMI and pay full cash upfront...

👉 You often receive the ₹10,000 discount directly, acquiring the product for just ₹90,000.

If you instead put the purchase on a standard credit card without converting it to an EMI and only pay the minimum amount due, you will fall directly into the classic Indian credit card debt trap, paying upwards of 40% annualized interest.

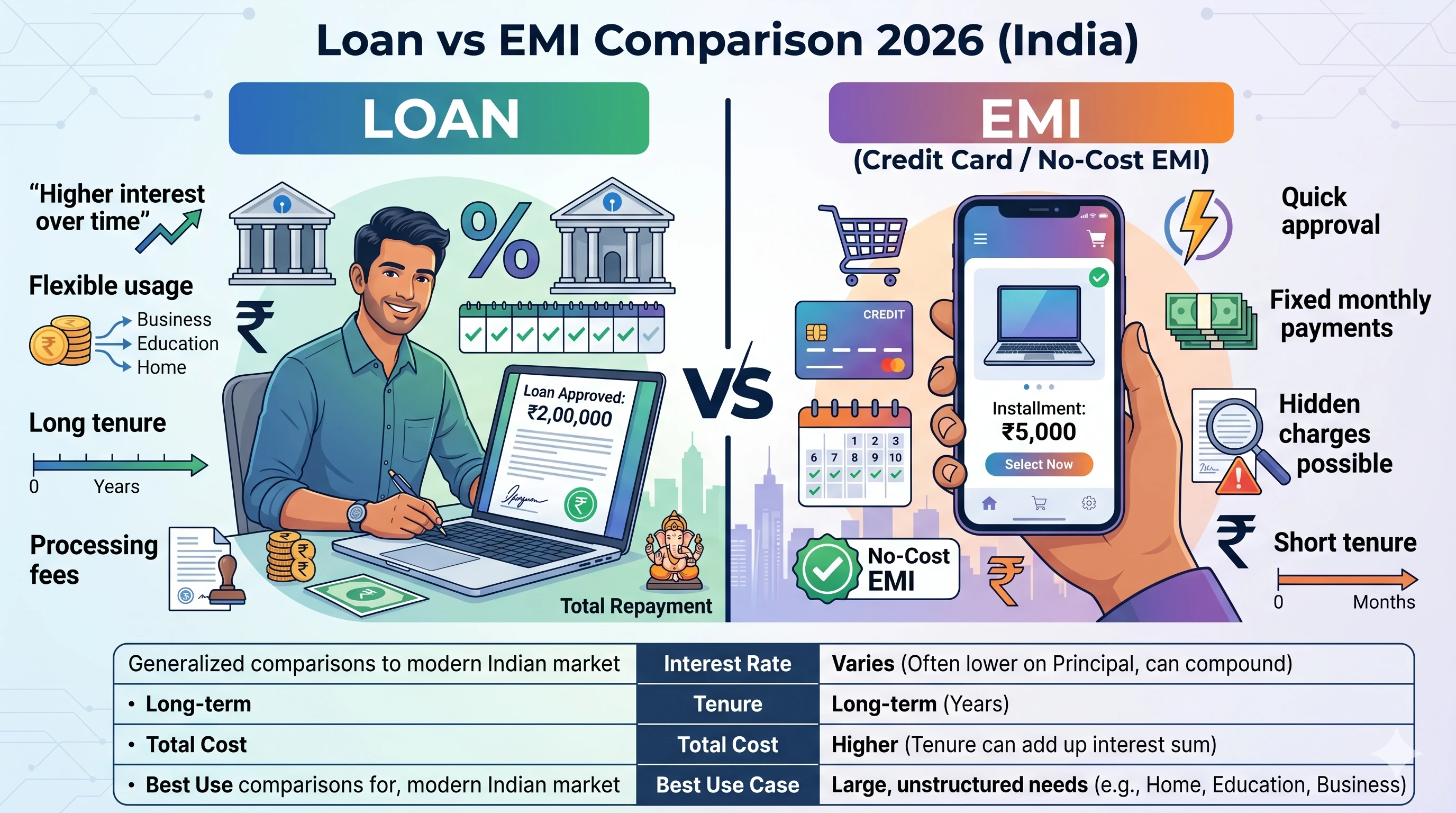

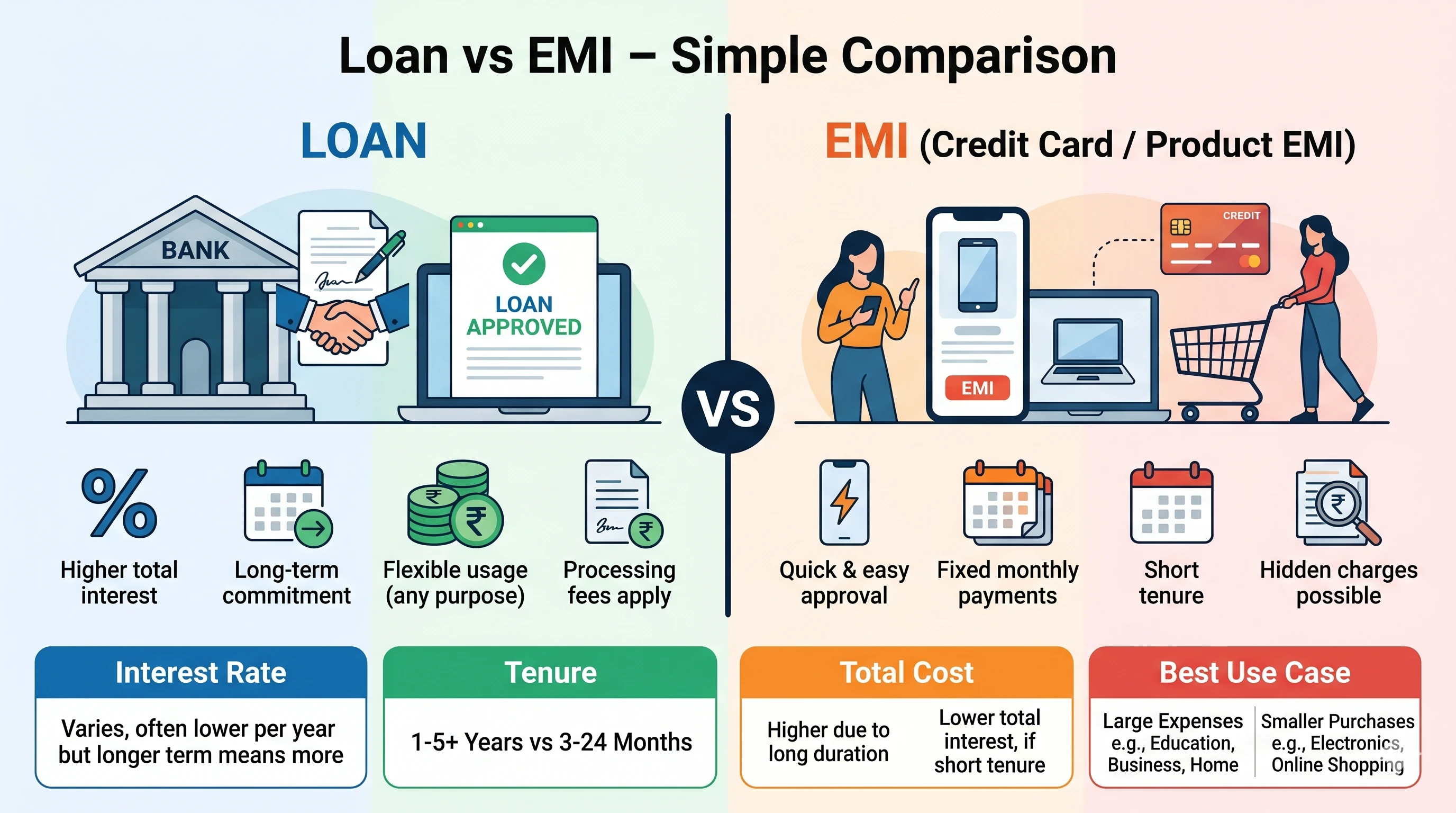

Personal Loan vs No-Cost EMI: Which One Actually Saves You Money?

⚠️ Most people choose wrong here and lose ₹5,000–₹20,000 in hidden fees.

👉 Always calculate your exact outflow before deciding.

While a No-Cost EMI is tied to a specific merchant purchase, a Personal Loan deposits raw cash into your bank account, offering unrestricted flexibility.

| Feature | Personal Loan | No-Cost EMI |

|---|---|---|

| Interest Rate | 10.5% to 24% p.a. (Paid fully by you) | 14% to 16% p.a. (Subsidized by merchant) |

| Processing Fees | 1% to 3% of total loan amount | Fixed nominal fee (₹199 - ₹999) |

| Fund Usage | Unrestricted (Medical, Travel, Debt) | Restricted to a specific product purchase |

| GST Impact | Applicable on Processing Fees only | Applicable on Processing Fees AND Interest |

- Buying a specific product: Choose No-Cost EMI

- Need direct cash: Choose Personal Loan

- Have existing credit card debt: Avoid both, consolidate first

Final Verdict: Which Should You Choose?

The choice between these two financing options boils down to the purpose of your borrowing.

Choose a No-Cost EMI if: You are purchasing electronics or consumer durables from a partnered retailer. Even with the hidden GST and processing fees, having the retailer subsidize the base interest makes it mathematically cheaper than drawing a fresh personal loan.

Choose a Personal Loan if: You need cash for medical emergencies, wedding expenses, or to consolidate high-interest credit card debt. A personal loan provides the liquidity required to negotiate cash discounts with vendors directly.

If you do take a personal loan, remember to implement step-up payments—a strategy to increase your EMI slightly every year with your salary increment—to become debt-free years ahead of schedule. Maintaining strict discipline with these payments will also dramatically increase your CIBIL score over time.

Frequently Asked Questions

Are No-Cost EMIs genuinely 0% interest?

No. The Reserve Bank of India bans 0% interest schemes. The merchant discounts the interest upfront, but you will still be charged a processing fee and 18% GST on the interest component by the bank.

Which is cheaper: Personal Loan or No-Cost EMI?

For buying specific consumer goods, a No-Cost EMI is mathematically cheaper because the merchant subsidizes the base interest. However, for generalized cash needs or debt consolidation, a personal loan is required.

🚀 Calculate Your Savings

Don't guess your monthly payments. Run the numbers on your exact loan amount.

Related Finance Guides