Most Indians Fall Into These 10 Credit Card Traps (Avoid Now)

⚠️ Paying only the minimum due can turn a ₹1 lakh balance into a ₹2.2 lakh debt. Most Indians don’t realize this until it’s too late.

The Indian credit card landscape has undergone a radical transformation over the last decade. (If you're already struggling with high interest payments, you must first read how to reduce your EMI burden by 40%). As we navigate through 2026, the sheer accessibility of credit has reached unprecedented levels. With the aggressive integration of RuPay credit cards on the Unified Payments Interface (UPI) network, scanning a QR code at a local street vendor and paying with borrowed money is now as frictionless as sending a WhatsApp message. While this convenience is a marvel of modern financial technology, it has inadvertently laid a perilous trap for millions of consumers.

Keeping up with relentless lifestyle inflation—fueled by social media, aggressive marketing, and the "Buy Now, Pay Later" (BNPL) culture—has driven an entire generation into a vicious debt spiral. Credit cards, when used with discipline, are exceptional financial tools that offer interest-free credit periods, robust fraud protection, and lucrative reward ecosystems. However, when treated as an extension of one's income rather than a short-term payment mechanism, they become weapons of wealth destruction.

If you are already scouring the internet for ways to reduce your existing EMI burdens, the misuse of credit cards will only exacerbate your financial hemorrhage. In this comprehensive guide, we will dissect the most devastating credit card mistakes Indians are making today, the hidden mathematics behind banking penalties, and actionable strategies to safeguard your financial future.

- Minimum due trap: Paying only 5% leads to a 40%+ annualized interest penalty.

- Credit limit rule: Keep your credit usage below 30% to protect your CIBIL score.

- Strictly avoid: ATM cash withdrawals, rent payments via cards, and closing old accounts.

👉 Want to see your exact interest accumulation? Calculate your credit card debt recovery plan here.

1. The Minimum Amount Due Trap: A One-Way Ticket to Financial Ruin

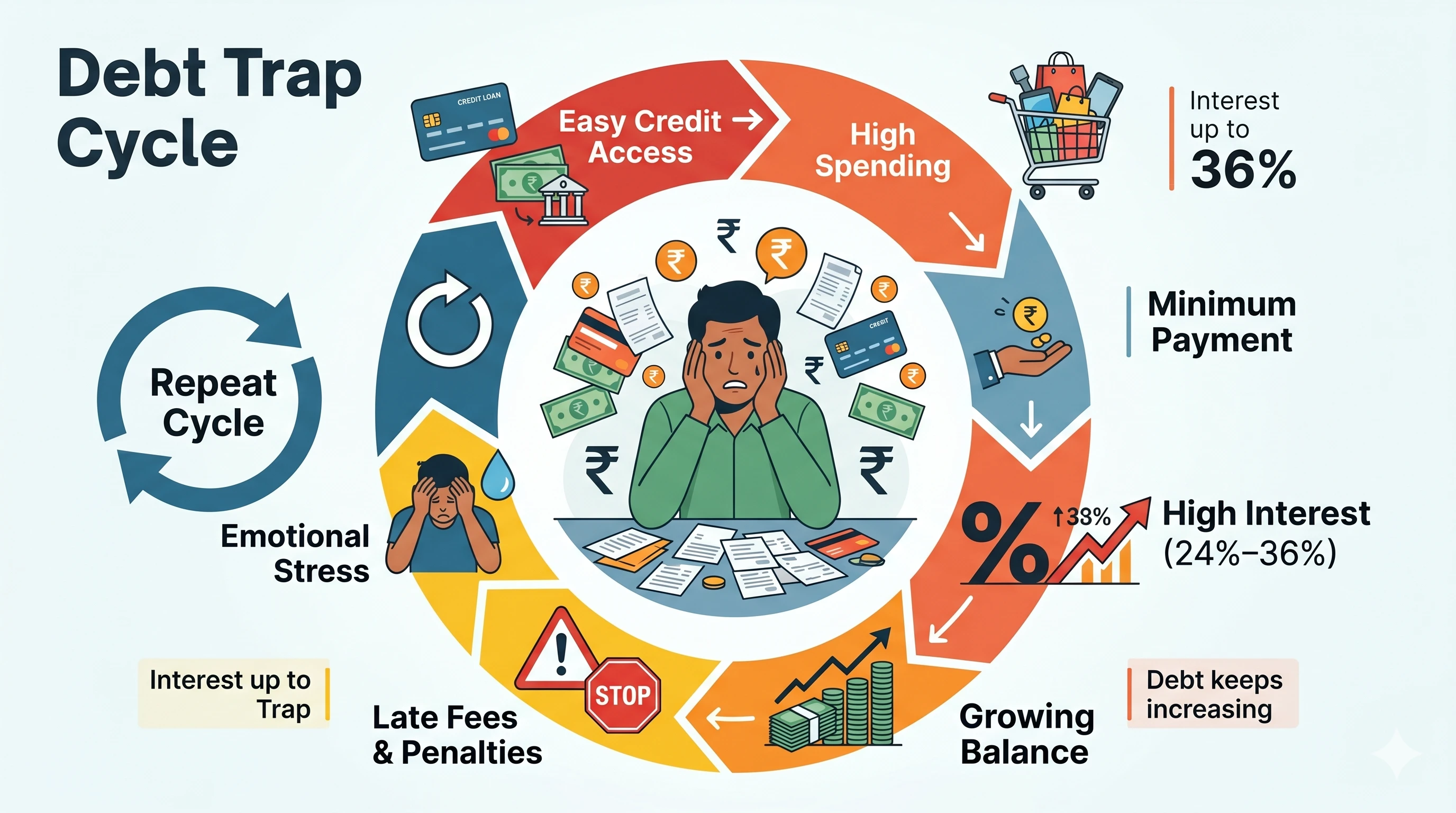

Perhaps the most widespread and financially lethal misunderstanding among Indian credit card users is the concept of the "Minimum Amount Due" (MAD). When your monthly statement arrives, the bank prominently highlights two figures: the Total Amount Due and the Minimum Amount Due. The MAD is typically calculated as 5% of your outstanding balance, plus any applicable EMIs and taxes.

To the untrained eye, paying the MAD feels like fulfilling your obligation to the bank. It keeps your account in "good standing" and prevents late payment fees. However, this is exactly where the illusion takes hold. Paying only the MAD is not a safe harbor; it is a financial quicksand.

The Horrifying Math of Revolving Credit

When you pay only the Minimum Amount Due, two catastrophic things happen immediately:

- Loss of the Interest-Free Grace Period: The moment you roll over a balance, your 45-to-50-day interest-free period is instantly revoked. Not only is interest charged on the remaining unpaid balance, but every new purchase you make from that day forward will instantly attract interest from the moment you swipe the card.

- Exorbitant Annualized Interest Rates (APR): Credit cards in India typically charge an interest rate (finance charge) of 3.5% to 4% per month. While 3.5% might sound harmless, compounding it monthly results in an Annual Percentage Rate (APR) of roughly 42% to 48%. This is among the highest interest rates of any legal financial product in the country.

| Payment Type | Interest Rate Applied | Financial Outcome |

|---|---|---|

| Full Statement Balance | 0% (Grace Period Active) | No debt, healthy CIBIL |

| Minimum Amount Due | 42% to 48% APR | Severe Debt Trap |

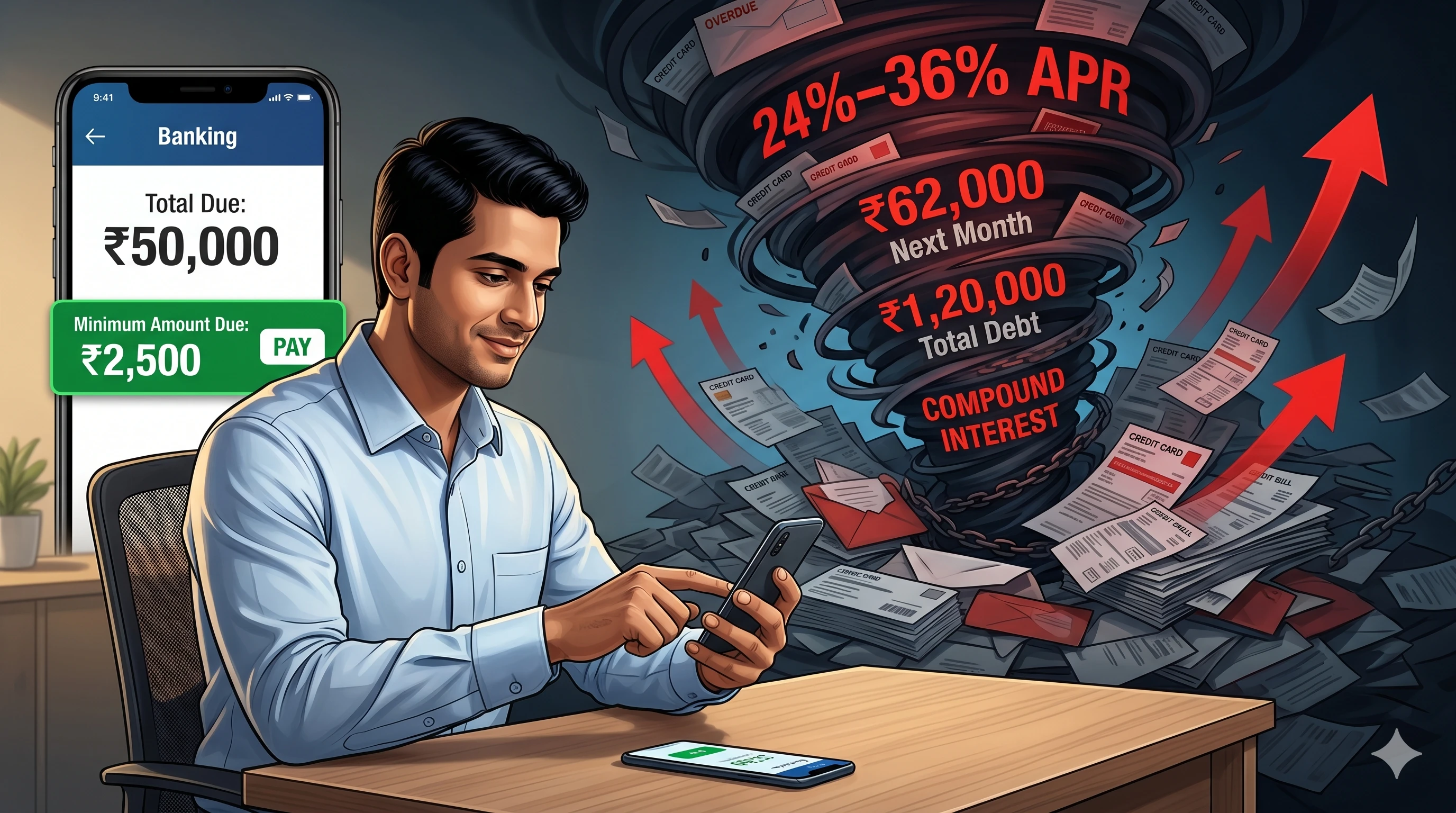

Let’s put this into perspective. Imagine you have an outstanding bill of ₹1,00,000. You decide to pay the 5% minimum due, which is ₹5,000. You now owe ₹95,000. At a modest 3.5% monthly interest rate, the bank will add ₹3,325 in interest to your next statement, completely wiping out the majority of the ₹5,000 payment you just made. Furthermore, an 18% Goods and Services Tax (GST) is levied on that interest component. If you continue paying only the minimum amount due without making any new purchases, it will literally take you over a decade to clear that ₹1,00,000 debt, and you will end up paying more than double the original amount to the bank.

| Initial Debt | Paying Only Minimum (5%) | Total You Eventually Pay |

|---|---|---|

| ₹1,00,000 | ₹5,000 / month | ₹2,20,000+ |

⚠️ If you have ₹1,00,000 debt and pay only the minimum due...

👉 You may end up paying ₹2,20,000+ in total to the bank.

2. Ignoring This 30% Rule Can Destroy Your CIBIL Score

Your Credit Information Bureau (India) Limited (CIBIL) score is the bedrock of your financial identity. It dictates your eligibility for home loans, car loans, and premium credit cards, as well as the interest rates you will be offered. One of the most heavily weighted factors in the CIBIL algorithm—accounting for roughly 30% of your total score—is your Credit Utilization Ratio (CUR).

The CUR is the percentage of your total available credit limit that you are currently using. For example, if you have a single credit card with a limit of ₹1,00,000 and your outstanding statement balance is ₹40,000, your CUR is 40%.

The 30% Golden Rule

Financial experts universally recommend keeping your credit utilization below 30%. When you consistently utilize 60%, 80%, or max out your credit cards, you send a glaring red flag to credit bureaus and lenders. It signals "credit hunger"—a desperate reliance on borrowed funds to sustain your lifestyle. Even if you pay your total bill in full and on time every single month, a consistently high CUR will actively suppress your CIBIL score.

If your CIBIL score drops due to high utilization, it ruins your chances of securing a favorable interest rate when you genuinely need to apply for a Personal Loan for a medical emergency or property purchase. To manage your CUR effectively, you can either spread your expenses across multiple credit cards, request a credit limit enhancement from your bank, or make mid-cycle payments before your statement is generated to artificially lower the reported outstanding balance.

3. The ATM Cash Advance Catastrophe (Instant 40%+ Penalty)

In a tight spot, walking up to an ATM and withdrawing cash using your credit card might seem like a convenient lifeline. In reality, it is one of the most expensive financial blunders you can make.

Unlike retail purchases, which enjoy an interest-free grace period of up to 50 days, cash advances have zero grace period. The moment the ATM dispenses the cash, the meter starts running. You will immediately be hit with a flat cash advance fee (typically 2.5% of the withdrawn amount or a minimum of ₹500, whichever is higher). On top of this fee, the standard 3.5% to 4% monthly interest rate begins compounding daily from day zero until the amount is paid in full. When you factor in the 18% GST on all these fees and interest charges, a seemingly innocent ₹10,000 cash withdrawal can easily cost you an extra ₹1,000 within the first billing cycle alone.

4. The "No-Cost EMI" Illusion: You Are Still Paying Interest

E-commerce giants and offline electronics retailers aggressively push "No-Cost EMI" schemes to incentivize the purchase of expensive smartphones, laptops, and appliances. The premise sounds magical: break down a ₹60,000 purchase into six monthly installments of ₹10,000 without paying a single rupee in interest. But in the world of finance, there are no free lunches.

The Reserve Bank of India (RBI) strictly prohibits banks from offering zero-percent interest loans. To circumvent this regulation and offer "No-Cost EMIs," merchants and banks use a clever discounting mechanism. Here is how it actually works:

- The bank still charges its standard interest rate for the EMI conversion (usually 14% to 16% annually).

- To offset this interest, the merchant provides an upfront discount equivalent to the total interest that will be charged over the tenure.

- For a ₹60,000 phone, the merchant might bill your card ₹57,000. The bank then adds ₹3,000 in interest over the next six months, bringing your total outflow back to ₹60,000.

While the core math seems to balance out, consumers consistently overlook two hidden financial drains. First, banks charge a non-refundable "EMI Processing Fee" (ranging from ₹199 to ₹999) simply to convert the transaction. Second, you are required to pay 18% GST on the interest component of every single EMI. Because the merchant discounted the principal, you are still legally obligated to pay the government tax on the bank's interest. Therefore, a "No-Cost EMI" always costs more than paying the upfront cash price.

In 2026, this trap is even more aggressive. AI-driven banking apps use hyper-personalization to send you targeted push notifications offering "1-Click EMI Conversions" or pre-approved personal loans mere minutes after a large transaction. They deliberately nudge you when your financial anxiety is high, hoping you convert a purchase you could have easily paid in full into a multi-month interest trap.

If you are considering a large purchase, we strongly recommend checking our No-Cost EMI comparison guide or calculating your exact monthly outflow directly using our Free EMI Tool to see the true cost before committing.

👉 Confused about how much GST you are paying on those hidden bank fees?

5. Why Closing Your Oldest Credit Card is a Huge Mistake

As you progress in your career and upgrade your lifestyle, it is common to acquire premium credit cards that offer superior lounge access, better reward multipliers, and travel milestones. In an attempt to declutter their wallets, many Indians make the mistake of closing their very first, entry-level credit cards.

Closing an old credit card hurts your CIBIL score in two distinct ways. First, it instantly reduces your total available credit limit, which mathematically spikes your Credit Utilization Ratio (as discussed in point #2). Second, it negatively impacts your "Average Age of Accounts" (AAoA). Credit bureaus favor borrowers with a long, stable history of credit management. Your oldest card acts as the anchor for your credit history. When you close it, that extensive history eventually falls off your report, lowering your overall score.

Instead of closing an old card just to avoid an annual fee, call your bank's retention department and ask them to convert the card to a "Lifetime Free" (LTF) variant. Keep the card active by using it for a minor recurring subscription, like a ₹99 streaming service, and set it to auto-pay. If your debt is already out of hand across multiple cards, explore our guide on strategic debt consolidation strategies rather than haphazardly closing accounts.

6. The Reward Point Trap: Spending ₹50,000 to Save ₹1,000

Credit card reward programs are meticulously designed using behavioral economics to make you spend more than you normally would. The gamification of spending—where you are promised 10,000 bonus points or a free domestic flight ticket if you spend ₹4,00,000 in a calendar year—often leads to severe lifestyle inflation.

Many consumers fall into the trap of manufacturing spends just to hit a milestone. They might buy expensive gadgets they don't need or offer to pay for group dinners just to rack up points. However, the intrinsic value of reward points has been heavily devalued by Indian banks over the past few years. A point that used to be worth ₹1.00 might now be worth ₹0.25 when redeemed for statement credit, or restricted to a highly inflated specific catalog of products.

Spending ₹50,000 extra just to earn a voucher worth ₹1,000 is mathematically absurd, yet thousands fall for this illusion daily. Furthermore, reward points are completely forfeited if you default on your payments. The overarching rule is simple: optimize your card usage for the spending you were already going to do, never spend to optimize your card.

7. The International Travel Disaster: Hidden Forex & DCC Fees

International travel has surged post-pandemic, and Indians are swiping their domestic credit cards in Dubai, Europe, and Southeast Asia more than ever. What most travelers fail to read in the fine print is the Foreign Currency Markup fee.

When you swipe a standard Indian credit card abroad, the bank charges a Forex Markup fee typically ranging from 3.5% to 4%. Because this is a fee for a financial service, the government adds 18% GST on top of the markup. This means every time you buy a coffee or pay a hotel bill overseas, you are paying nearly 4.5% extra purely in banking fees.

Even more insidious is the Dynamic Currency Conversion (DCC) trap. When you swipe your card at an international merchant, the point-of-sale machine will often ask, "Would you like to pay in your home currency (INR) or the local currency?" Paying in INR feels safe because you immediately know the exact amount you are spending. However, selecting INR triggers DCC. The merchant's acquiring bank sets a notoriously terrible exchange rate—often 5% to 7% worse than the actual market rate—and your home bank will still charge a DCC markup fee. The golden rule of international travel is to always choose to pay in the local currency of the country you are visiting, and ideally use a zero-forex markup credit card.

8. Why Delaying Your Payment by "Just One Day" Costs You Thousands

In the era of instant digital notifications, forgetting a credit card due date shouldn't happen, but it does. Consumers often rationalize a missed payment by thinking, "It's just one day late, I'll pay it tomorrow."

The RBI mandates that banks must give a 3-day grace period after the due date before reporting a default to CIBIL or charging late payment fees. However, relying on this grace period is a dangerous game. If a technical glitch delays your NEFT or IMPS transfer, you will cross that threshold. Once you do, the consequences are severe:

- A hefty Late Payment Fee is levied (which can be up to ₹1,300 depending on the outstanding balance), plus 18% GST.

- The 3.5% monthly interest rate is applied to the entire outstanding balance from the date of the original transactions, not just from the due date.

- A missed payment mark is etched into your CIBIL report, remaining visible to future lenders for up to 36 months, devastating your credit score.

Always set up an auto-debit mandate from your primary savings account for the "Total Amount Due" 3 to 5 days before the actual deadline.

9. The Hidden 4% Penalty on Credit Card Rent Payments

Between 2021 and 2024, a massive trend emerged in India: using third-party fintech apps to pay house rent to landlords using credit cards. The appeal was obvious—you could meet high annual spending milestones, earn reward points, and enjoy a 45-day interest-free loan on your biggest monthly expense.

Banks quickly realized they were bleeding money on these transactions and clamped down hard. Today, using a credit card to pay rent is a massive financial mistake. The fintech app will charge a convenience fee of 1.5% to 2%. Then, your bank will levy its own "Rent Payment Surcharge" of 1% to 1.5%. Add the 18% GST on all these fees, and you end up paying an extra 3% to 4% on your rent every single month. To make matters worse, almost all major Indian banks have excluded rent payments from earning any reward points or contributing to milestone benefits. You are literally paying extra fees for zero return.

10. The Silent Killer: Never Checking Your Itemized Monthly Statement

The final, and perhaps most common, mistake is treating the credit card statement as a simple notification of the amount due, rather than an itemized financial ledger. Most consumers glance at the Total Amount Due, pay it via an app like CRED or Cheq, and archive the email.

Failing to review your itemized statement line-by-line leaves you vulnerable to hidden charges. In 2026, "subscription creep" is a massive issue. Free trials for software, streaming services, or premium delivery apps automatically convert into recurring monthly charges that go entirely unnoticed. Additionally, banks are notorious for quietly slipping in charges for "Card Protection Plans," insurance policies you never explicitly agreed to, or annual fees that were supposed to be waived.

Make it a non-negotiable monthly ritual to spend 5 minutes reviewing your statement. If you spot an unrecognized charge, you have a limited window (usually 30 to 60 days) to raise a dispute and initiate a chargeback.

Frequently Asked Questions

Is paying the Minimum Amount Due bad?

Yes. Paying only the minimum amount revokes your interest-free grace period and subjects your remaining balance and new purchases to an APR of 42% to 48%, keeping you in a debt trap for years.

What is a good Credit Utilization Ratio (CUR)?

Financial experts recommend keeping your Credit Utilization Ratio below 30% of your total available credit limit to maintain a healthy CIBIL score.

Are No-Cost EMIs really free of interest?

No. The RBI prohibits zero-interest loans. In a No-Cost EMI, the merchant discounts the interest upfront, but you still pay a non-refundable EMI processing fee and 18% GST on the interest component.

Conclusion: Mastering the Plastic

Credit cards are the double-edged swords of personal finance. They can build your credit profile, fund your vacations through rewards, and protect you from fraud. But the moment you slip into the habit of paying the minimum amount due, ignoring your utilization ratios, or funding a lifestyle you cannot afford, they become instruments of financial ruin.

The path to financial freedom in 2026 requires hyper-vigilance. Pay your total bill in full, never withdraw cash from an ATM with a credit card, scrutinize the math behind No-Cost EMIs, and treat your credit limit as a tool of convenience, not an emergency fund. If you are struggling to manage existing debt, start by calculating your exact liabilities using our Free EMI Tool and read our comprehensive 40% EMI Reduction Plan to take back control of your financial destiny.

🚀 Next Step: Create Your Escape Plan

If you're already in debt, read our proven strategy to Reduce Your EMI Burden by 40%.

👉 Instead of paying compound interest to the bank, let compound interest work for you! Plan your wealth creation.

Related Guides